|

|

THE ACCOUNTANTS (EXAMINATIONS) RULES

ARRANGEMENT OF RULES

PART I – PRELIMINARY

PART II – EXAMINATIONS RULES

| 5. |

Registration requirements

|

| 6. |

Booking of examinations

|

| 7. |

Allocation of examination centres

|

| 9. |

Conduct of students in the examination room

|

| 10. |

Rules on computer based examinations

|

| 11. |

Time allotted for examination sittings

|

| 12. |

Intellectual property of examination materials

|

| 13. |

Examination centre coordinator

|

| 16. |

Proctoring invigilators for computer-based examination centres and online remote proctored centres

|

| 19. |

Courier service providers

|

| 21. |

Action for breach of the examination rules

|

| 22. |

Examination investigation

|

| 24. |

Short vocational programmes

|

| 25. |

Certificate programmes

|

| 27. |

Professional examinations

|

| 28. |

Post graduate Diploma Training

|

| 29. |

Exemption and equation of certificates

|

| 32. |

Duration of registration as a student

|

| 33. |

Renewal fees for a continuing student

|

| 34. |

Deferment of examinations

|

| 37. |

Examinations Board right to retain answer scripts or templates

|

| 38. |

Development and review of syllabuses

|

| 39. |

Issue of certificates

|

| 40. |

Promotion of the recognition of the examinations of the Examinations Board in foreign countries

|

| 41. |

Promotion of the publication of books and other materials relevant to examinations of the Examinations Board

|

PART III – ACCREDITATION GUIDELINES

| 42. |

Accreditation Standards

|

PART IV – TRANSITIONAL PROVISIONS

| 43. |

Transitional Provisions

|

SCHEDULES

| FIRST SCHEDULE [r. 6(1)] — |

REGISTRATION/EXEMPTION/EXAMINATION BOOKING

|

| SECOND SCHEDULE [r. 23] — |

OATH OF SECRECY ON EXAMINATIONS

|

| THIRD SCHEDULE [r. 36(2)] — |

REMARKING APPEAL FORM

|

| FOURTH SCHEDULE [r. 42(1)] — |

APPLICATION FORM FOR ACCREDITATION OF TRAINING INSTITUTIONS

|

| FIFTH SCHEDULE [r. 42(13)] — |

ACCREDITATION FEE

|

THE ACCOUNTANTS (EXAMINATIONS) RULES, 2022

PART I – PRELIMINARY

| 1. |

Citation

These Rules may be cited as the Accountants (Examinations) Rules, 2022.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires —

“agent” means a person either natural or artificial not being a member of staff, appointed by the Examinations Board to undertake examinations related assignments from time to time;

"accreditation" means the formal recognition and confirmation by certification that an institution has met and continues to meet the quality standards of, training and competence set by the Examinations Board in liaison with the Ministry of Education in accordance with the guidelines set out in Part III of these Rules;

“area coordinator “means an officer appointed by the County Education Officer to manage, control and handle all the examination related matters of the Examinations Board at the sub-county level during the administration of examinations;

“attempt timer” means a clock indicating the time limit for starting the examination offered by the Examinations Board;

"Cabinet Secretary" has the meaning assigned to it under section 2 of the Act;

“candidate” means a natural person who has been registered by the Examinations Board and has been entered for an examination;

“chief invigilator” means an officer appointed by the Examinations Board to manage, control and handle all the examination related matters of the Examinations Board at the assigned examinations centre during the administration of examinations;

“computer-based examinations” means an examination that is conducted online through the use of internet or a computer-aided facility;

“Examinations Board” has the meaning assigned to it under section 2 of the Act;

“examination centre coordinator” means officer appointed by the Examinations Board and designated as an examinations centre coordinator to coordinate logistical matters at the examinations centre during the administration of an examination;

“examination materials” means any materials and or equipment made available by the Examinations Board to a candidate during an examination, including but not limited to examination question papers and examination answer booklets;

"examination timer" means a computer clock that shows current, start and finish time with countdown set in hours and minutes to let candidates know how much time is left while taking examinations;

"institution" means an institution accredited to offer training in subjects examinable by the Examinations Board;

"online remote proctored examinations" means computerized examinations conducted through Examinations Board’s online examination portal, during which a candidate is monitored virtually and in real time by an online proctor, and for which control and monitoring also takes place afterwards, on the basis of video and audio recordings made during the examination;

“online proctor” means a person tasked with invigilating online exams via Webcam;

“professionals’ examination” means any examination offered by the Examinations Board which is classified under category seven of qualification pathways issued by the Kenya National Qualifications Authority in accordance with the Kenya National Qualifications Framework Act or any other qualification set out by the International Federation of Accountants or any other regulatory body, locally or internationally;

“registered student” means a student who having met all the entry requirements set by the Examinations Board for any of its examinations, has been duly registered and has a registration number;

“supervisor” means an employee of the Examinations Board or employee of Government deployed to monitor the conduct and administration of examinations within a given examination centre or group of centres;

“technicians’ examination” means any examination offered by the Examinations Board which is below the professional examination and includes but is not limited to vocational, certificate and diploma examinations; and

“webcam” means a video camera that feeds or streams an image or video in real time to or through a computer to a computer network, such as the internet.

|

| 3. |

Objects and purpose

The objects and purpose of these Rules is to govern matters relating to the administration, management and conduct of examinations offered by institutions and accreditation of institutions by the Examinations Board in accordance with the Act.

|

PART II – EXAMINATIONS RULES

| 4. |

Scope of the Rules

These Rules provide for the following —

| (a) |

development and review of syllabi for examinations offered by the Examinations Board;

|

| (b) |

accreditation of institutions offering training in subjects examinable by the Examinations Board;

|

| (c) |

administration, management and conduct of examinations of the Examinations Board;

|

| (d) |

examinations’ irregularities and the penalties thereof;

|

| (e) |

issuance of certificates by the Examinations Board;

|

| (f) |

exemption and equation of certificates including prescribing what examinations may be equated by the Examinations Board in liaison with the Commission for University Education, Technical and Vocational Education and Training Authority, Kenya National Qualifications Authority or any other relevant statutory body;

|

| (g) |

examination fees and other charges payable to the Examinations Board; and

|

| (h) |

approval of publication of books and other materials relevant to examinations offered by the Examinations Board.

|

|

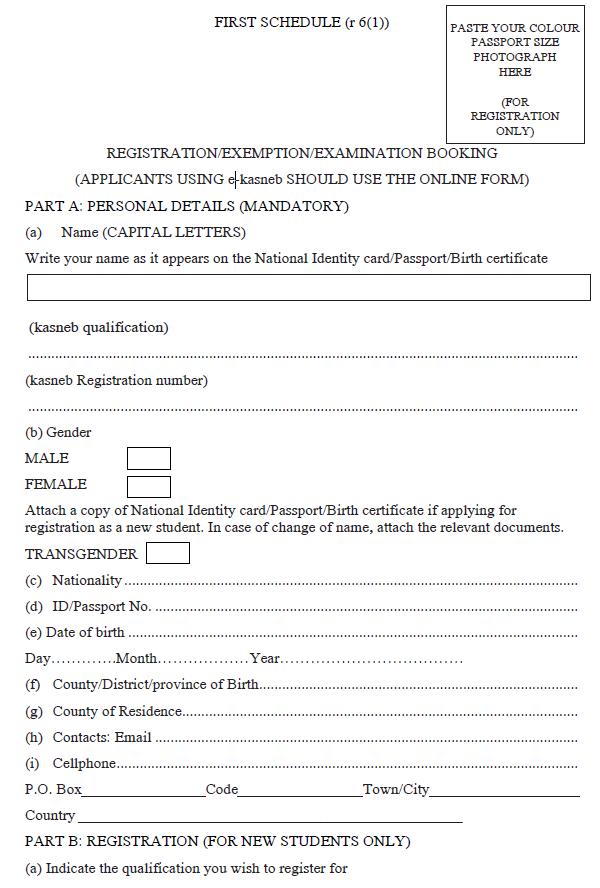

| 5. |

Registration requirements

| (1) |

A person shall be deemed to have been registered as a candidate upon meeting all the entry requirements set out in these Rules and paying the registration fees.

|

| (2) |

A birth certificate shall suffice for identification purposes for registration until a candidate acquires a national identification or any other recognized document for identification.

|

| (3) |

The Examinations Board has the right to reject any application for registration for a justifiable reason.

|

|

| 6. |

Booking of examinations

| (1) |

An examination entry, which shall be in the form set out in the First Schedule, shall be accepted from a registered student.

|

| (2) |

The Examinations Board shall assign each candidate a registration number upon registration as a student of the Examinations Board.

|

| (3) |

The closing date for the receipt of entries for the various examination sittings shall be determined by the Examinations Board from time to time.

|

| (4) |

Notwithstanding the provisions of sub rule (3), the Examinations Board may extend the date of students’ registration under special circumstances.

|

| (5) |

Where the Examinations Board extends the closing date under sub rule (4), the Examinations Board —

| (a) |

shall allow adequate time for the administration of the examination;

|

| (b) |

may charge additional fees for any such late entries; and

|

| (c) |

shall keep a record of the students registered under special circumstances.

|

|

| (6) |

Once registered students have been entered for a particular examination sitting, a summary of all the registered students shall be tabled to the Board.

|

| (7) |

The Examinations Board shall circulate the register of students to the designated chief invigilator before the commencement of the particular examination sitting.

|

| (8) |

In each examination sitting, the Examinations Board shall, upon approval by the Board under sub rule (4), transmit a list of all newly registered students entered for the certified public accountant examination to the Institute, on or before twenty-one days after closure of the register.

|

|

| 7. |

Allocation of examination centres

| (1) |

The Examinations Board shall assess and identify appropriate centres for each examination sitting of the Examinations Board.

|

| (2) |

A registered student who has been entered for an examination, may select three or such other number of examination centres as may be determined by the Examinations Board in the order of priority for consideration and allocation by the Examinations Board.

|

| (3) |

The Examinations Board shall allocate examination centres to students who apply under sub rule (2) based on capacity and availability of the centres.

|

| (4) |

Despite sub rule (3), the Examinations Board shall reserve the right to transfer candidates from one centre to another centre, for the efficient administration of examinations.

|

| (5) |

Where the Examinations Board transfers a candidate to another examination centre under sub rule (4), the Examinations Board shall communicate such transfer to the candidate in writing within forty-eight hours or any other time, in the event of an emergency before an examination commences.

|

|

| 8. |

Examination sittings

| (1) |

The Examinations Board shall determine the number of examination sittings in each year and reserves the right to reschedule any or all examination sittings.

|

| (2) |

Where the Examinations Board reschedules an examination sitting under sub rule (1), the Examinations Board shall notify the affected candidates and the public within reasonable time.

|

|

| 9. |

Conduct of students in the examination room

The following rules shall govern the conduct of students in the examination room —

| (a) |

a candidate shall present himself for an examination at least thirty minutes before the scheduled time for the commencement of the examination he or she is taking;

|

| (b) |

a candidate shall identify himself or herself before being allowed to sit an examination by presenting his national identification or any other document approved by the Board to sit an examination;

|

| (c) |

a candidate who arrives more than half an hour after the commencement of an examination shall not be allowed to take the examination;

|

| (d) |

a candidate shall not be permitted to leave the examination room until after the end of the first half hour from the commencement of an examination provided that a chief invigilator may remove a candidate who is disruptive, less than the first half hour from such commencement;

|

| (e) |

a candidate shall sit at the place indicated by the assigned registration number in the examination room;

|

| (f) |

a candidate shall indicate his registration number on the answer sheet;

|

| (g) |

a candidate shall not insert his name on the answer sheet;

|

| (h) |

each answer sheet shall have a serial number indicated on the top, left hand side;

|

| (i) |

a candidate shall indicate the serial number of the answer sheet used for each examination paper in the signature register;

|

| (j) |

the Examinations Board shall provide stationery in the examination room, but candidates shall bring their own blue or black ink pens, pencils, rulers or any other materials or equipment approved by the Examinations Board;

|

| (k) |

electronic devices and other equipment including but not limited to mobile phones, pagers, laptops, e-readers, tablets, smart watches or any other devices capable of transmitting, storing or receiving information whether internet connected or otherwise, electronic equipment capable of being programmed to hold alphabetical or numerical data or formulae, shall not be allowed in the examination room unless otherwise approved by the Examinations Board;

|

| (l) |

no stationery shall be removed from the examination room for physical examinations, except that which a candidate is permitted to bring into the examination room;

|

| (m) |

a candidate shall not use calculators unless such calculators are noiseless, cordless and non-programmable unless approved by the Examinations Board;

|

| (n) |

a candidate shall observe strict silence and shall not cause any form of disturbance during the entire duration of the examination;

|

| (o) |

a candidate shall not possess any notes, printed paper or books in the examination room;

|

| (p) |

a candidate using a clipboard shall ensure that such clipboard has no writing and the chief invigilator, who confirms that a candidate’s clipboard has any writing, shall disqualify the candidate from taking the examination;

|

| (q) |

smoking shall not be allowed in the examination room;

|

| (r) |

no food or drinks shall be allowed in the examination room;

|

| (s) |

a candidate shall not collude in the examination room with any other candidate or agents of the Examinations Board;

|

| (t) |

during the course of the examination, no candidate shall leave the examination room without permission from the chief invigilator and any candidate who does so will not be allowed to return to the examination room;

|

| (u) |

a candidate who finishes an examination before the chief invigilator announces the end of the examination and wishes to leave the examination room while the examination is in progress shall inform the invigilator and hand in his or her scripts to the chief invigilator before leaving the examination room;

|

| (v) |

notwithstanding paragraph (u), no candidate shall be allowed to leave the examinations room during the last fifteen minutes of the examination;

|

| (w) |

a candidate shall not leave the examination room with any answer booklet or answer sheets;

|

| (x) |

a candidate shall not leave the examination room before his answer booklets and the question paper are collected by the invigilators;

|

| (y) |

a candidate shall not write notes on the examination timetable;

|

| (z) |

a candidate shall not write on the examination question papers;

|

| (aa) |

a candidate with confirmed disability and registered with the National Council for Persons with Disabilities, may apply to the Examinations Board to be allowed extra time during the examinations;

|

| (bb) |

an application under paragraph (aa) shall be made at least two months prior to the examination and shall include the relevant supporting evidence as may be determined by the Examinations Board from time to time; and

|

| (cc) |

a candidate shall not carry weapons inside the examination room.

|

|

| 10. |

Rules on computer based examinations

The following rules shall govern the conduct of computer based examinations —

| (a) |

subject to rule 9, the Examinations Board may administer computer-based examinations;

|

| (b) |

where the Examinations Board administers a computerbased examination, the Examinations Board shall set up examination centres for that purpose or use any other method approved by the Examinations Board;

|

| (c) |

where a computer-based examination is being administered virtually or remotely, the Examinations Board shall have power to determine devices which can be attached to the candidate’s computer for purposes of monitoring the administration of the examination;

|

| (d) |

where there is an examination centre for computer-based examinations, the Examinations Board shall ensure that —

| (i) |

a candidate has access to internet connection during the examination; |

| (ii) |

the examinations centre has a conducive environment for taking an examination; |

| (iii) |

the candidate observes all conditions set out in these Rules; |

| (iv) |

the candidates are given clear instructions by the invigilators throughout the examination; |

| (v) |

the needs of persons with disabilities are taken into account before selection of a computer-based examination centre; |

| (vi) |

all computer-based examinations are commenced and completed at the scheduled time; and |

| (vii) |

no one Internet Protocol address is used simultaneously to take an examination; |

|

| (e) |

a candidate taking an online remote proctored examination shall prove his or her identity prior to the examination by—

| (i) |

taking a photograph of himself or herself with the webcam, with the face being fully visible; and |

| (ii) |

taking a photograph with the webcam of a valid proof of identity including a closely resembling photograph; |

|

| (f) |

for online remote proctored examinations, a candidate shall show the test environment by making a 360° film of the test environment with the webcam; and the film must enable the invigilator to check whether the environment is in line with the following requirements —

| (i) |

the candidate’s test environment is quiet and tranquil; |

| (ii) |

there shall not be any other people in the room; |

| (iii) |

the desk or other workplace, shall only have a computer and, in case the computer does not have an internal webcam, an external web camera; |

| (iv) |

notwithstanding sub paragraph (iii), only explicitly permitted materials for instance photo ID, email with link and activation code and books shall be allowed during open-book Examinations; |

| (v) |

there shall not be sounds like music from any device or any other sounds; |

| (vi) |

there shall not be other computers or similar devices running in the examination room; and |

| (vii) |

lighting shall be “daylight" quality and overhead light is preferred, where possible. |

|

| (g) |

during the Examination, the candidate’s conduct shall meet the following requirements —

| (i) |

the attempt timer and the examination timer shall begin once the invigilator has entered the PIN or PASSWORD, and the candidate clicks on the ‘Start attempt’ button or icon; |

| (ii) |

a candidate shall not navigate away from the exam screen, unless authorized by the invigilator; |

| (iii) |

during the examination, a candidate is not allowed to use any other applications save for Examinations Board’s registration tool, the examination and monitoring software made available by Examinations Board and an e-mail application accompanied by an examination code to be used during the exam; |

| (iv) |

a candidate may not leave the room after starting the examination and before submitting the examination answer template; |

| (v) |

a candidate shall face the computer screen during the Examination; |

| (vi) |

a candidate shall not take screen shots during the Examination; |

| (vii) |

a candidate is not allowed to surf on the internet or to consult digital data or web pages or to have these opened, unless this is expressly permitted; |

| (viii) |

a candidate shall not wear ear plugs or headphones unless where permitted by the Examinations Board for special cases; |

| (ix) |

a candidate shall dress and behave decently at all times; |

| (x) |

a candidate shall not receive assistance from the invigilator, or anyone else, during the examination; |

| (xi) |

a candidate shall not ask the invigilator questions except where there are technical issues with the examination platform; |

| (xii) |

a candidate shall not make noise of any nature during the examination session; |

| (xiii) |

only the examination material supplied by the Examinations Board during the examination may be used; |

| (xiv) |

where the use of books during the examination is allowed pursuant to the examination requirements, the candidate must show the book by means of a video recording and the video recording shall enable the invigilator to assess whether the requirements have been met; and |

| (xv) |

where a candidate is allowed to use a book under sub paragraph (xiv), the candidate shall at least show the front and back covers of the book and shall browse the book slowly. |

|

| (h) |

the following rules shall govern the use of and set-up of electronic devices for the administration of computer based examinations —

| (i) |

a computer shall not have a desktop sharing software installed and activated on the computer; |

| (ii) |

the webcam and microphone required for the examination shall be enabled and running for the duration of the examination; |

| (iii) |

the webcam shall be focused at all times on the candidate taking the Examination; |

| (iv) |

a candidate's face shall be positioned within the limits permitted by the Examinations Board; and |

| (v) |

a candidate shall not tamper with the lens of the webcam at any time during the examination. |

|

| (i) |

the Examinations Board may approve the installation of any device in a computer based examination for purposes of administration of the examination;

|

| (j) |

the Examinations Board shall put in place procedure manuals to guide the administration of computer-based examinations.

|

|

| 11. |

Time allotted for examination sittings

| (1) |

Every examination shall be completed within the allocated time.

|

| (2) |

In the case of computer-based examinations —

| (a) |

examinations shall be submitted within the time allotted before the online examination timer expires; and

|

| (b) |

once the examination timer expires, the exam shall be automatically submitted.

|

|

|

| 12. |

Intellectual property of examination materials

| (1) |

All rights, including the copy rights and other intellectual property rights that can be exercised with regard to the examination materials, shall vest exclusively with the Examinations Board and its licensors.

|

| (2) |

Notwithstanding sub rule (1) a candidate may only use the examination materials in so far as this is necessary for taking an examination.

|

| (3) |

The Examinations Board shall avail past examination papers online for access by registered students and accredited training institutions for revision purposes, at a fee to be determined by the Examinations Board.

|

| (4) |

The Examinations Board may grant access to past examination papers to trainers and scholars for research purposes or any other person approved by the Examinations Board, at a fee to be determined by the Examinations Board.

|

| (5) |

A candidate may collect his or her question paper twenty four hours after an examination, at no cost.

|

|

| 13. |

Examination centre coordinator

The roles of an examination centre coordinator shall be to —

| (a) |

liaise with the area coordinator from the county education office;

|

| (b) |

provide a room where the chief invigilator will keep examination materials, question papers and answer scripts or any other examination materials;

|

| (c) |

ensure that there are adequate facilities for the administration of the examination, including rooms, halls, desks and chairs;

|

| (d) |

ensure a conducive environment in the examinations room;

|

| (e) |

liaise with the chief invigilator as necessary; and

|

| (f) |

perform any other duties assigned by the Examinations Board necessary for the efficient administration of examinations

|

|

| 14. |

Chief invigilators

The roles of an examination chief invigilator shall be to —

| (a) |

induct invigilators before the commencement of examinations;

|

| (b) |

receive the examination summary sheet from the Examinations Board;

|

| (c) |

collect examinations materials from a designated custody point on a daily basis during examinations and ensure the return of the examination materials at the end of each day;

|

| (d) |

ensure the safe custody of the examination materials under his or her jurisdiction at all times;

|

| (e) |

prepare a sketch sitting arrangement for every examination session;

|

| (f) |

ensure that the invigilators’ session roll is marked for every examination session;

|

| (g) |

ensure that all candidates are properly supervised during the conduct of the examinations;

|

| (h) |

announce the start and stop times in each examination room;

|

| (i) |

announce the time updates to candidates on an hourly basis in each examination session, including during the last one hour, when updates shall be announced on the 45th and 30th minutes;

|

| (j) |

manage and supervise the use of examination materials in the examinations room;

|

| (k) |

confirm that the number of scripts packed and the number labelled as packed are in agreement and shall thereafter sign on each envelope next to the invigilators’ signatures;

|

| (l) |

manage and supervise invigilators at the examination centre;

|

| (m) |

ensure that the candidates’ attendance registers are marked appropriately for every examination session and are submitted to the Examinations Board together with the answer scripts at the end of the examination period;

|

| (n) |

prepare an examination centre report at the end of the examination period showing all examination materials received, used and returned; and

|

| (o) |

perform any other lawful duties as may be assigned by the Examinations Board.

|

|

| 15. |

Invigilators

The roles of an examination invigilator shall be to —

| (a) |

ensure proper labelling of candidates’ sitting positions before each examination;

|

| (b) |

distribute examination materials to the candidates;

|

| (c) |

monitor the conduct of examinations in each examination room including collecting evidence of examination malpractice;

|

| (d) |

collect examination materials from each candidate at the end of each examination session;

|

| (e) |

pack all examination materials after each examination session under the supervision of the chief invigilator;

|

| (f) |

report any incidences related to the conduct of examinations to the chief invigilator;

|

| (g) |

confirm the identity of candidates during each examination session;

|

| (h) |

ensure every candidate signs on the signature register and indicates the serial number of the answer booklet used; and

|

| (i) |

perform any other lawful duties as may be assigned by the Examinations Board.

|

|

| 16. |

Proctoring invigilators for computer-based examination centres and online remote proctored centres

The roles of an on line proctor shall be to —

| (a) |

safeguard all examination materials in his custody;

|

| (b) |

accurately identify the candidates by their national identification or any other methods authorized by the Examinations Board;

|

| (c) |

ensure unauthorized materials are removed, unless explicitly permitted by the Examinations Board;

|

| (d) |

ensure the examination room is ready and conducive for examination before commencement of the examination;

|

| (e) |

monitor the candidate’s access to a stable, uninterrupted internet connection before the start of, and during the examination and report to the Examinations Board any instances of instability or interruption;

|

| (f) |

avail the PIN or PASSWORD to enable candidates to access and start the examinations;

|

| (g) |

monitor the conduct of examinations in each examination room using webcams or any other electronic devices approved by the Examinations Board;

|

| (h) |

time the examination and stop the computer-based examination after the lapse of the allocated time for the examination; and

|

| (i) |

perform any other lawful duties as may be assigned by the Examinations Board.

|

|

| 17. |

Area co-ordinator

The roles of an area coordinator shall be to —

| (a) |

liaise with the Examinations Board on examination matters during the conduct of examinations;

|

| (b) |

advise the Examinations Board on appropriate examination centres for each sitting;

|

| (c) |

nominate chief invigilators and invigilators for appointment by the Examinations Board for examination centres outside Nairobi but within the country;

|

| (d) |

receive and arrange for safe custody of examination materials from the agents of the Examinations Board;

|

| (e) |

collect examination materials from the Examinations Board’s agents during the conduct of the examinations of the Board;

|

| (f) |

liaise with chief invigilators and examination centre coordinators on examination matters during the conduct of the examinations;

|

| (g) |

make arrangements for return of examinations material to the examinations board after the conduct of examinations; and

|

| (h) |

perform any other lawful duties as may be assigned by the Examinations Board.

|

|

| 18. |

Banks and armouries

| (1) |

The Examinations Board may engage banks and armouries, as agents for purposes of providing logistics for storing examination materials.

|

| (2) |

Where the Examinations Board engages a bank or an armoury under sub-rule (1), the parties shall sign a service level agreement specifying the terms and conditions of each party.

|

| (3) |

Despite sub-rule (2), the roles of a bank or an armoury shall include —

| (a) |

receiving and accounting for all the examinations materials under their custody;

|

| (b) |

safeguarding all the examinations materials in their custody;

|

| (c) |

issuing the examinations materials to the area coordinators and supervisors upon positive identification;

|

| (d) |

upon completion of the examinations, receiving the examination materials from the area coordinators and supervisors upon positive identification;

|

| (e) |

releasing examinations materials to coordinators of the Examinations Board upon completion of the examinations;

|

| (f) |

updating the Examinations Board on any relevant incidences related to conduct of examination materials during the administration of the examinations; and

|

| (g) |

performing any other lawful duties as may be assigned by the Examinations Board.

|

|

|

| 19. |

Courier service providers

| (1) |

The Examinations Board may engage courier service providers, as agents for purposes of providing logistics for transporting examination materials.

|

| (2) |

Where the Examinations Board engages a courier services provider under sub-rule (1), the parties shall sign a service level agreement specifying the terms and conditions of each party.

|

| (3) |

Despite sub-rule (2), the service level agreement shall specify the roles of a courier service provider to include —

| (a) |

delivery of the examination materials to the designated delivery points;

|

| (b) |

preparing and maintaining relevant documents relating to the deliveries;

|

| (c) |

collecting examinations materials from designated points after the conduct of examinations and delivering them to the Head office of the Examinations Board; and

|

| (d) |

performing any other lawful duties as may be assigned by the Examinations Board.

|

|

|

| 20. |

Examination breaches

| (1) |

The Examinations Board shall take disciplinary action against candidates, Examinations Board’s agents or other parties who breach the examination rules of the Examinations Board.

|

| (2) |

A breach of these examination rules by the Examinations Board’s agents shall include —

| (a) |

altering or making unauthorised changes in the original answer script or template of a candidate without lawful authority by agents of the Examinations Board or any other party;

|

| (b) |

recklessly or negligently losing an examination paper, material or other information or using such examination paper, material or information by the Examinations Board’s agents in a manner prejudicial to the proper and fair conduct of any examination;

|

| (c) |

acting or inciting any other person to act in a disorderly manner;

|

| (d) |

taking away examination materials, including examination question papers, answer booklets or electronic devices from the examination room or any other designated place without authorization by the Examinations Board;

|

| (e) |

writing of names on the examination question paper, scripts or online template;

|

| (f) |

inducement of or an attempt to induce, solicit or influence the Examinations Board’s agents to gain advantage over the other candidates in an examination;

|

| (g) |

possession of unauthorized materials including mobile or any other unauthorised electronic devices in the examination room unless in circumstances approved by the Examinations Board;

|

| (h) |

taking away candidates scripts, examinations’ marking schemes or any unauthorized material from the examination marking centre; and

|

| (i) |

allowing other individuals, other than candidates and invigilators, to come in and out of the room during the examination.

|

|

| (3) |

A breach of these examination rules by a student shall include—

| (a) |

failure to provide required identification documents;

|

| (b) |

collusion with other candidates or agents of the Examinations Board;

|

| (c) |

acting or inciting any other person to act in a disorderly manner;

|

| (d) |

taking away examination materials, including examination question papers, answer booklets or electronic devices from the examination room without authorization by the Examinations Board;

|

| (e) |

writing of names on the examination question paper, scripts or online template; and

|

| (f) |

inducement of or an attempt to induce, solicit or influence the Examinations Board’s agents to gain advantage over the other candidates in an examination.

|

|

| (4) |

A breach of these examination rules by a publisher shall include —

| (a) |

publishing materials without the approval of the Examinations Board on subjects examinable by the Board, purporting to guide students on the syllabus, either physically or online; and

|

| (b) |

promoting published materials on subjects examinable by the Board without the approval of the Examinations Board.

|

|

|

| 21. |

Action for breach of the examination rules

| (1) |

The action for breach of these examination rules shall, in the case of a student, include the following —

| (a) |

de-registration as a student of the Examinations Board;

|

| (b) |

cancellation of registration number;

|

| (c) |

nullification of a candidate’s results for the particular examination sitting in dispute;

|

| (d) |

prohibition from taking examinations of the Examinations Board for a period to be determined by the Examinations Board;

|

| (e) |

written reprimand or warning; and

|

| (f) |

report to the law enforcement agencies for appropriate action.

|

|

| (2) |

An agent of the Examination Board who breaches any of these examination rules shall be —

| (a) |

barred from invigilating the examinations of the Examinations Board;

|

| (b) |

reported to the employer or regulator for administrative action;

|

| (c) |

barred from marking examinations of the Examinations Board; and

|

| (d) |

reported to the law enforcement agencies for appropriate action.

|

|

| (3) |

Where a publisher breaches the examination rules —

| (a) |

the Examinations Board shall publish in the print media notices denouncing the published examination information;

|

| (b) |

the Examinations Board shall publish in the print media, lists of examination materials approved by the Board for publication; and

|

| (c) |

the Examinations Board shall report such matter to the law enforcement agencies for appropriate action;

|

|

| (4) |

Where an employee of the Examinations Board breaches the examination rules, the employee shall be subjected to disciplinary procedures in accordance with the existing policies of the Examinations Board.

|

| (5) |

Where the Examinations Board is satisfied that there has been an irregularity in the course of any examination, the Examinations Board shall suspend or nullify such examination or any part thereof.

|

| (6) |

Where the Examinations Board is satisfied that there is reasonable cause to believe that the examination results of any candidate have been obtained by irregular means, the Examinations Board shall nullify the examination results of such candidate.

|

| (7) |

In the exercise of its powers under this rule, the Examinations Board may —

| (a) |

conduct such investigations as it may deem necessary; and

|

| (b) |

during such investigations, withhold the examination results of a candidate pending conclusion of the investigations.

|

|

|

| 22. |

Examination investigation

| (1) |

In the course of the investigations under rule 21, the Examinations Board may call for such information or the production of such documents as the Examinations Board may require, within such period and in such form and place as the Board may determine, from such person as the Examinations Board may determine, to assist in the investigations.

|

| (2) |

The Examinations Board may at its discretion refer certain breaches of these rules to the relevant law enforcement agencies for appropriate action.

|

| (3) |

A candidate shall be accorded an opportunity to defend himself or herself in relation to the evidence provided regarding the examinations’ breaches.

|

|

| 23. |

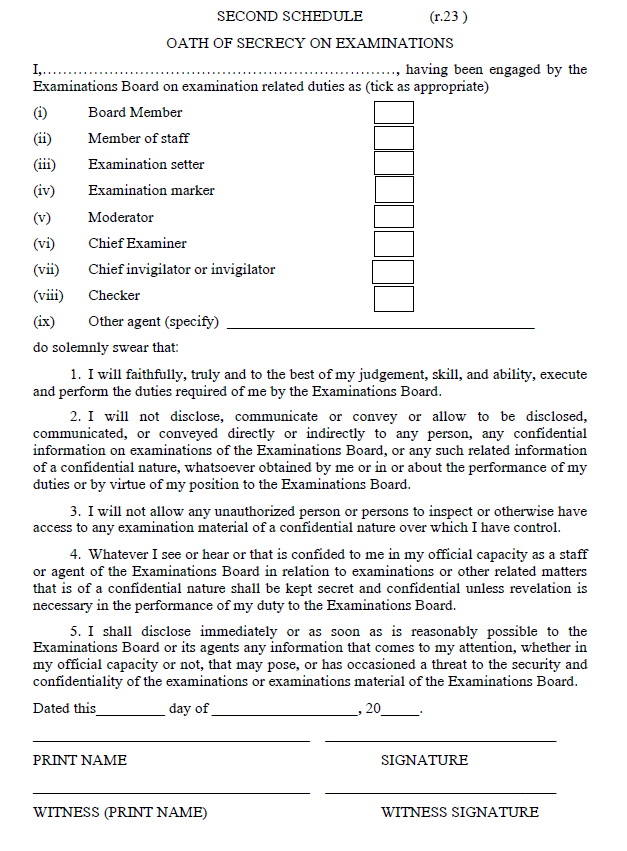

Oath of secrecy

The Examinations Board shall require a Board member, agent or staff performing the work of the Examinations Board, engaged in the conduct of any examination or the handling of any examination paper or material, to take and subscribe the oath of secrecy set out in the Second Schedule.

|

| 24. |

Short vocational programmes

A person seeking to be registered as a student of the Examinations Board for short vocational programmes shall meet the requirements determined by Kenya National Qualifications Authority or any other relevant body and adopted by the Examinations Board for the vocational course.

|

| 25. |

Certificate programmes

A person seeking to be registered as a student for the certificate programme administered by the Examinations Board, shall meet the requirements determined by Kenya National Qualifications Authority or any other relevant body and adopted by the Examinations Board for a certificate course in a tertiary institution.

|

| 26. |

Diploma programmes

A person seeking to be registered as a student for a diploma programme administered by the Examinations Board, shall meet the requirements determined by Kenya National Qualifications Authority or any other relevant body and adopted by the Examinations Board for a diploma course in a tertiary institution.

|

| 27. |

Professional examinations

| (1) |

A person seeking to be registered as a student for the professional programme administered by the Examinations Board shall meet the requirements determined by the professional institutes, Kenya National Qualifications Authority or any other relevant body and adopted by the Examinations Board for admission to a university for a degree course.

|

| (2) |

A candidate shall meet the subject combination determined by the Examinations Board.

|

|

| 28. |

Post graduate Diploma Training

| (1) |

A person seeking to be registered as a student for a post graduate diploma programme administered by the Examinations Board, shall meet the requirements determined by Kenya National Qualifications Authority or any other relevant body and adopted by the Examinations Board for a post graduate course.

|

| (2) |

Where a post graduate diploma training is in the area of accountancy, the Examinations Board shall seek the advice of the Institute.

|

|

| 29. |

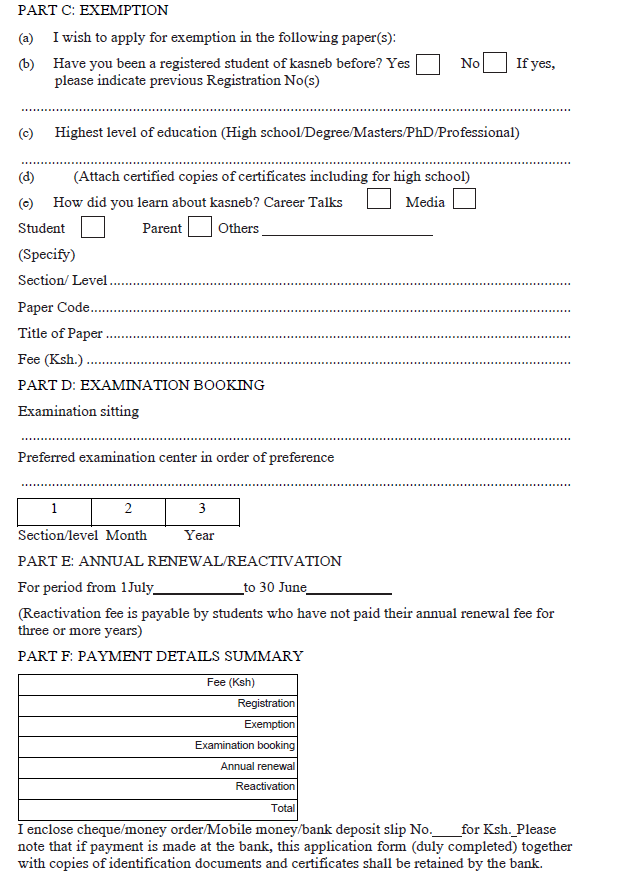

Exemption and equation of certificates

| (1) |

The Examinations Board may, on application by a registered student who holds a degree, diploma, professional or any other qualification recognized by the Examinations Board, grant an exemption to such student at a fee determined by the Examinations Board.

|

| (2) |

For the purpose of granting an exemption under sub-rule (1), the Examinations Board may equate other certificates issued by other national or foreign examination bodies to its certificates.

|

| (3) |

The Examinations Board may consult with the ministry responsible for foreign affairs, the Kenya National Qualification Authority, Commission for University Education or such other regulatory bodies as deemed appropriate for purposes of equating certificates.

|

|

| 30. |

Code of Conduct

A prospective candidate shall be required to execute the Code of Conduct of the Examinations Board upon registration.

|

| 31. |

Charging of fees

| (1) |

The Examinations Board shall charge such fees as necessary for the discharge of its mandate as determined by the Examinations Board

|

| (2) |

Such fees shall include registration, examination entry, exemption, annual renewal fees and any other additional fees as may be determined by the Examinations Board from time to time.

|

|

| 32. |

Duration of registration as a student

| (1) |

A registered student of the Examinations Board shall complete examinations within a period not exceeding —

| (a) |

one year, in the case of short courses;

|

| (b) |

three years, in the case of certificate courses;

|

| (c) |

six years, in the case of diploma courses;

|

| (d) |

ten years, in the case of professional courses; and

|

| (e) |

three years, in the case of post-qualification courses.

|

|

| (2) |

The periods in sub rule (1) shall commence on the date of registration.

|

| (3) |

The Examinations Board reserves the right to cancel the registration of a student who fails to complete the examination within the period set out in sub rule (1).

|

|

| 33. |

Renewal fees for a continuing student

| (1) |

A registered student shall renew his or her registration annually on the first day of July in each year or any other time as determined by the Examinations Board.

|

| (2) |

A student who fails to renew the registration for three consecutive years shall have his or her registration number deactivated.

|

| (3) |

The Examinations Board may upon satisfaction readmit a student whose number had been deactivated under sub rule (2), subject to the payment of —

| (a) |

a registration reactivation fee;

|

| (b) |

arrears of annual renewal fees; and

|

| (c) |

the current year’s renewal fees.

|

|

| (4) |

The Examinations Board may exempt a student from any payments under sub rule (3) who had given notice to the Examinations Board in writing and the Board had approved the deferment.

|

|

| 34. |

Deferment of examinations

| (1) |

A registered student may defer registration for an examination sitting subject to the circumstances and conditions approved by the Examinations Board for deferment.

|

| (2) |

A registered student who has registered for an examination sitting may only defer a sitting once and only to the next sitting.

|

| (3) |

An application for deferment under sub-rule (2) shall be received by the Examinations Board not later than thirty days before the examinations date, or such other period as may be specified by the Deferment of examinations.

|

|

| 35. |

Examination results

| (1) |

The Examinations Board shall avail the examinations results within a reasonable time following completion of each examination.

|

| (2) |

The Examinations Board shall avail the examinations results via text messages and on the Examinations Board’s student portal or in whatever other format as may be determined by the Examinations Board from time to time.

|

| (3) |

The Examinations Board reserves the right to use the examinations scripts or templates and submitted materials for training and feedback purposes.

|

|

| 36. |

Remarking

| (1) |

A candidate, who has failed an examination paper and is dissatisfied with the results of his performance, may apply for a review of his results in writing to the Secretary to the Examinations Board and shall pay such a fee as may be determined by the Examinations Board from time to time.

|

| (2) |

Such an application must be in the form set out in the Third Schedule and within two weeks from the date of release of examination results or a period determined by the Examinations Board under special circumstances.

|

|

| 37. |

Examinations Board right to retain answer scripts or templates

| (1) |

The Examinations Board shall not return any examination scripts or templates to a candidate or his agents.

|

| (2) |

The Examinations Board shall retain the examinations scripts or templates for at least three months from the date of releasing the examination results, unless there is a pending court case.

|

| (3) |

Where there is a court case, the Examinations Board shall retain the examinations script or template until the court case is conclusively determined.

|

|

| 38. |

Development and review of syllabuses

| (1) |

The Examinations Board shall after every five years or any other such period as the Examinations Board may determine from time to time, undertake a major review of syllabuses for professionals’ and technicians’ examinations in accountancy and company secretarial practice and related disciplines.

|

| (2) |

The Examinations Board may on an annual basis undertake a minor review of the syllabuses for professionals’ and technicians’ examinations in accountancy and company secretarial practice and related disciplines.

|

| (3) |

During the review processes, the Examinations Board shall –

| (a) |

seek the advice of the Institute on matters relating to examinations standards and policies pursuant to section 9(d) of the Act;

|

| (b) |

seek the advice of the Institute of Certified Investment and Financial Analysts with regard to investment and financial analysts’ examinations pursuant to section 8 of the Investment and Financial Analysts Act, (No. 13 of 2015);

|

| (c) |

seek the advice of the Institute of Certified Public Secretaries of Kenya with regard to certified secretaries’ examinations pursuant to section 7 (d) of the Certified Public Secretaries of Kenya Act, (Cap. 534); and

|

| (d) |

consult other key stakeholders, including the Government, professional bodies, employers, training institutions and students.

|

|

| (4) |

The Examinations Board shall prepare protocols to guide the transition from the old syllabuses to the new syllabuses.

|

| (5) |

The Examinations Board shall communicate within a reasonable time regarding the revised syllabuses for professionals’ and technicians’ examinations in accountancy and company secretarial practice and related disciplines and protocols to the students, the public and other stakeholders.

|

|

| 39. |

Issue of certificates

| (1) |

The Examinations Board shall determine the period for printing examinations certificates for the immediate last sitting for issuance to the students and may vary the period based on

circumstances from time to time.

|

| (2) |

The Examinations Board shall communicate within a reasonable time to a registered student or graduate for the collection of his certificate.

|

| (3) |

A registered student or graduate shall collect his or her certificate in person at the offices of the Examinations Board.

|

| (4) |

Where a registered student or graduate is unable to collect his or her certificate in person at the offices of the Examinations Board, the student or graduate shall provide in writing, a reliable address for the postage of the certificate by registered mail and attach a copy of his national identification documents or such other identification documents approved by the Examinations Board.

|

| (5) |

The Examinations Board may provide a period within which the certificates are to be collected free of any storage charge, and any storage charge applicable upon expiry of such period.

|

|

| 40. |

Promotion of the recognition of the examinations of the Examinations Board in foreign countries

| (1) |

The Examinations Board shall collaborate with other relevant institutions in other countries including but not limited to government agencies, training institutions and professional bodies to promote the recognition of its examinations in foreign countries by —

| (a) |

establishing liaison offices in foreign examination or regulatory institutions;

|

| (b) |

signing mutual recognition agreements or memorandums of understanding with foreign examination or regulatory institutions jointly with the Institute; and

|

| (c) |

assessing and accrediting training institutions in foreign countries to offer training in subjects examinable by the Examinations Board.

|

|

| (2) |

The Examinations Board shall make policies to promote the recognition of examinations of the Examinations Board in any foreign country which has cordial diplomatic relations with Kenya.

|

| (3) |

In pursuit of the recognition of the examinations of the Examinations Board in such foreign countries, the Examinations Board may lobby through the relevant foreign governments and agencies for the employment of its graduates, under the guidance of the ministry responsible for foreign affairs.

|

|

| 41. |

Promotion of the publication of books and other materials relevant to examinations of the Examinations Board

| (1) |

The Examinations Board may engage subject-matter experts who may include members of professional bodies to develop relevant books and other materials relevant for its examinations.

|

| (2) |

Notwithstanding sub rule (1), the Examinations Board may recommend books written by other parties for publication and use by its students.

|

| (3) |

Before recommending any book referred to in sub rule (2), the Examinations Board shall undertake a review of such a book and may charge such fee as may be determined by the Examinations Board for undertaking such review.

|

| (4) |

No publisher shall publish materials purporting to prepare candidates for examinations of the Examinations Board without the approval of the Examinations Board.

|

|

PART III – ACCREDITATION GUIDELINES

| 42. |

Accreditation Standards

| (1) |

An institution intending to offer training in subjects examinable by the Examinations Board in Kenya, shall apply to the Examinations Board in the form set out in the Fourth Schedule.

|

| (2) |

An application under this Part shall be accompanied by a statement setting out the following particulars —

| (a) |

the name, physical, postal and electronic addresses of the institution;

|

| (b) |

the governance and management structures of the institution;

|

| (c) |

membership of the institution;

|

| (d) |

aims and objectives for which the institution has been established and the programmes of instruction and courses of study that are to be offered;

|

| (e) |

the number, qualifications and competence of the manager and trainers;

|

| (f) |

layout designs and specifications of available infrastructure and equipment;

|

| (g) |

a statement on the suitability, ownership or lease arrangement for premises as evidence of the structural soundness of buildings and capacity in accordance with the Public Health Act (Cap. 242)

|

| (h) |

a statement of financial ability and fees to be charged; and

|

| (i) |

such other information as may be required by the [Examnination Board.

|

|

| (3) |

The Examinations Board shall, within such period as it may determine, after the receipt of an application under sub rule (2)—

| (a) |

examine the documents submitted; and

|

| (b) |

inspect and assess the facilities available for use in respect of the institution.

|

|

| (4) |

The Examinations Board shall make a detailed accreditation report and return it to the applicant.

|

| (5) |

Where the Examinations Board is satisfied that the institution meets the conditions for accreditation, the Examinations Board shall enter the particulars of the institution in its register and issue the institution with a certificate to offer training in the form determined by the Examinations Board.

|

| (6) |

Where the Examinations Board is of the opinion that the application does not meet the conditions for the accreditation, it may —

| (a) |

reject the application; or

|

| (b) |

advise the applicant to make the necessary adjustments or modifications to meet the threshold set by the Examinations Board.

|

|

| (7) |

Where the Examinations Board issues an advisory sub rule (6)(b), the applicant may submit a revised application within a period of six months.

|

| (8) |

Upon receipt of a revised application under sub rule (7), the Examinations Board shall make a decision and if satisfied, accredit the institution in accordance with these Rules.

|

| (9) |

The Examinations Board shall maintain a register indicating the particulars of institutions accredited under the Act and these Rules.

|

| (10) |

The register under sub rule (9) shall be open for inspection by members of the public during office hours free of charge or be available on the Examinations Board’s website.

|

| (11) |

The Board shall grant two types of accreditation based on the extent of compliance by an institution with the set standards —

| (a) |

interim accreditation for a period of eighteen months; or

|

| (b) |

full accreditation for a period of five years.

|

|

| (12) |

Where an accredited institution does not meet the set standards during subsequent assessment, the Examinations Board may consider the following further action —

| (a) |

withdrawal of accreditation for a period to be specified by the Examinations Board;

|

| (b) |

require the institution to provide a comprehensive compliance plan; or

|

| (c) |

withdraw the accreditation certificate, where the institution fails to implement the comprehensive compliance plan submitted under paragraph (b) within the timelines set out therein.

|

|

| (13) |

The Examinations Board shall charge the fees set out in the Fifth Schedule for the assessment of accreditation.

|

| (14) |

Pursuant to rule (2)(e), a trainer shall hold —

| (a) |

relevant qualifications related to the subject and level or part of the examination in which he or she provides training;

|

| (b) |

a qualification that is one level above the qualification for which he or she provides training as prescribed by the relevant authority on qualifications;

|

|

| (15) |

A trainer for professional level examinations shall be required to have a professional qualification and an undergraduate degree.

|

| (16) |

A trainer for specialised courses which the Examinations Board does not offer professional qualifications shall be required to hold a relevant undergraduate degree in the area of specialization.

|

| (17) |

| (a) |

shall be registered with the relevant professional bodies governing their field of specialisation and be in good standing; or

|

| (b) |

shall be required to undertake relevant courses as may be determined by the Examinations Board from time to time, where a relevant professional body is not in place; and

|

| (c) |

shall undertake a course on pedagogy and andragogy every year as determined by the Examinations Board in consultation with the relevant professional or academic institutions;

|

| (d) |

shall undergo refresher courses on emerging issues at least once a year or as determined by the Examinations Board in consultation with the relevant professional or academic institutions.

|

|

|

PART IV – TRANSITIONAL PROVISIONS

| 43. |

Transitional Provisions

| (1) |

All continuing students of the Examinations Board before the commencement of these Examinations Rules shall be deemed to be bona fide students for purpose of these Rules.

|

| (2) |

Any certificate of qualifications issued by the Examinations Board prior to the commencement of these Rules shall be deemed to have been issued under these Rules.

|

| (3) |

All decisions made relating to disciplinary issues and pending disciplinary matters before the Examinations Board shall be considered as valid upon commencement of these Rules.

|

| (4) |

The Oath of Secrecy shall become effective upon commencement of these Rules.

|

| (5) |

All institutions accredited by the Examinations Board shall retain their accreditation status upon commencement of these Rules for the unexpired period.

|

| (6) |

All exemptions granted by the Examinations Board at the commencement of these Rules shall be valid.

|

| (7) |

Any action or decision on examinations taken by the Examinations Board having effect before the commencement of these Rules, shall be deemed to have been done by the Examinations Board under these Rules.

|

|

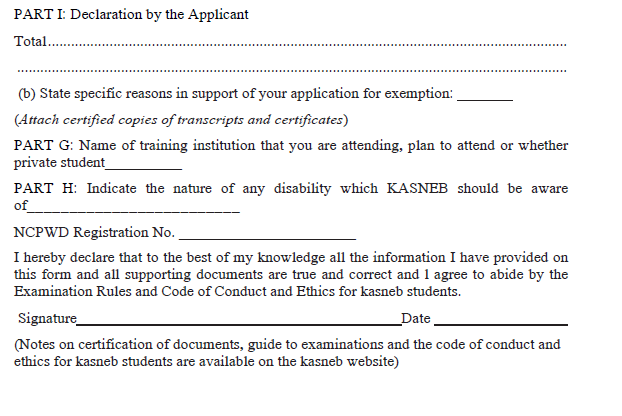

FIRST SCHEDULE [r. 6(1)]

REGISTRATION/EXEMPTION/EXAMINATION BOOKING

SECOND SCHEDULE [r. 23]

OATH OF SECRECY ON EXAMINATIONS

THIRD SCHEDULE [r. 36(2)]

REMARKING APPEAL FORM

Instructions to students

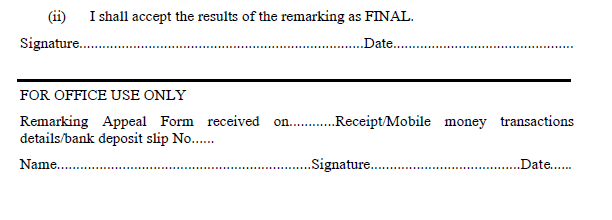

1. This form should be completed by students who wish to appeal for remarking of their examination paper(s). The form should be received by Kasneb within fourteen days after the date of release of the examination results. This date is indicated in the examination result notification. Students paying through the banks or other agents should personally send the forms attaching copies of deposit slips to Kasneb so as to be received within the stated deadline. Appeal forms received after the stated deadline will not be considered.

2. Students are ADVISED not to make the appeal decision in a rush and to note that no extraneous circumstances will be considered during the remarking.

3. The outcome of the appeal will be communicated to the student through the contact information provided on the form within four weeks of the appeal. Kasneb will NOT enter into any further correspondence with the student on the appeal.

4. Your name should NOT appear anywhere on this form.

5. The form should be delivered in person or sent by post. Email and other electronic media shall only be used where proof of payment is attached.

6. A remarking fee shall be charged at KSh.5,000.00 (US$50) per paper for technician and diploma level examinations and KSh.7,500.00 (US$75) per paper for professional level examinations.

7. You will be required to commit yourself to accept the outcome of the remarking as final.

8. You should attach a copy of the receipt, bank deposit slip or mobile money transactions details for the remarking fee.

FOURTH SCHEDULE [r. 42(1)]

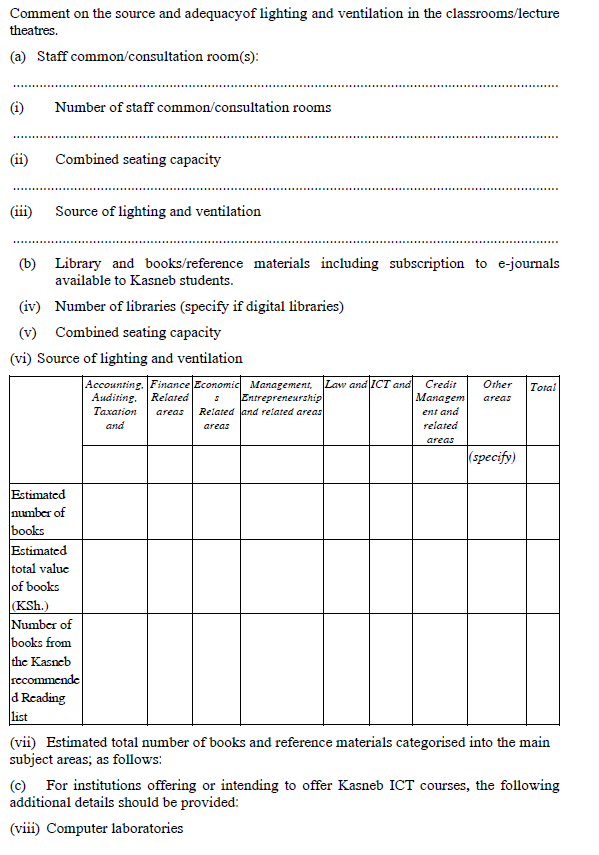

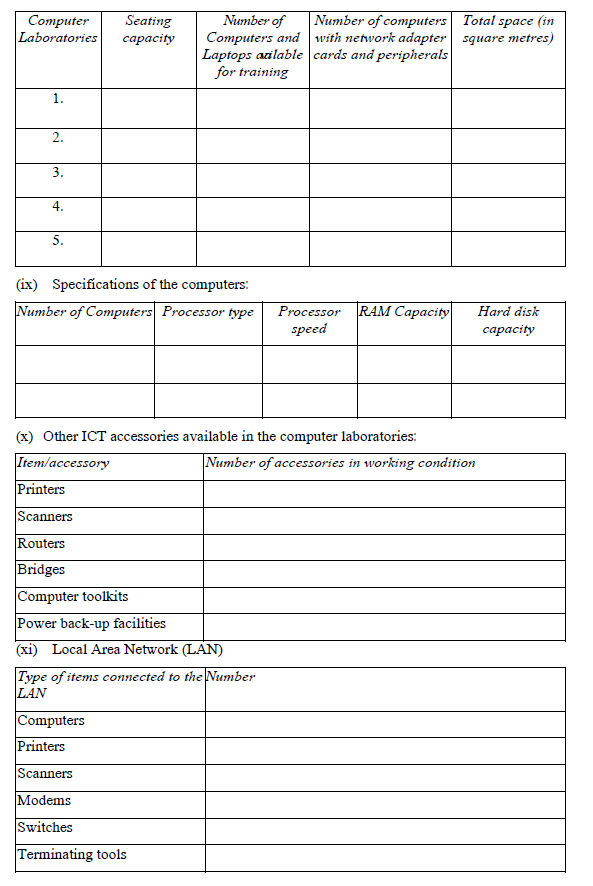

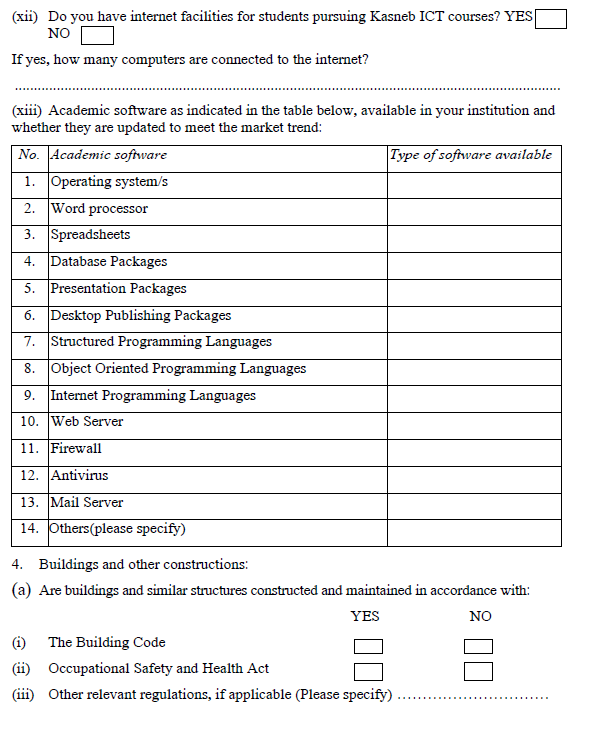

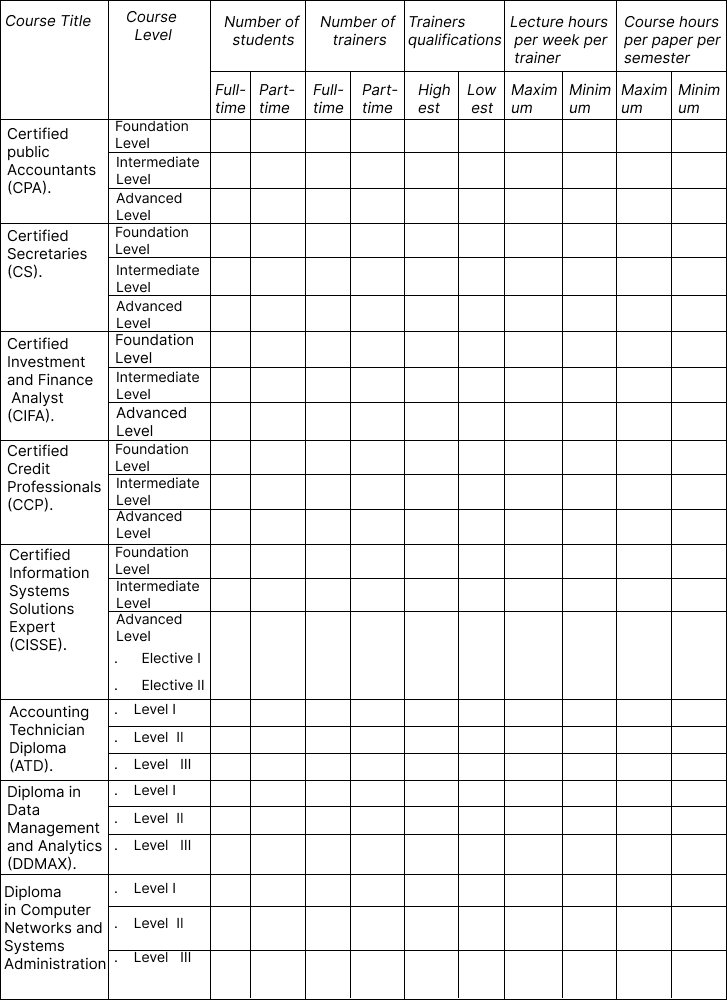

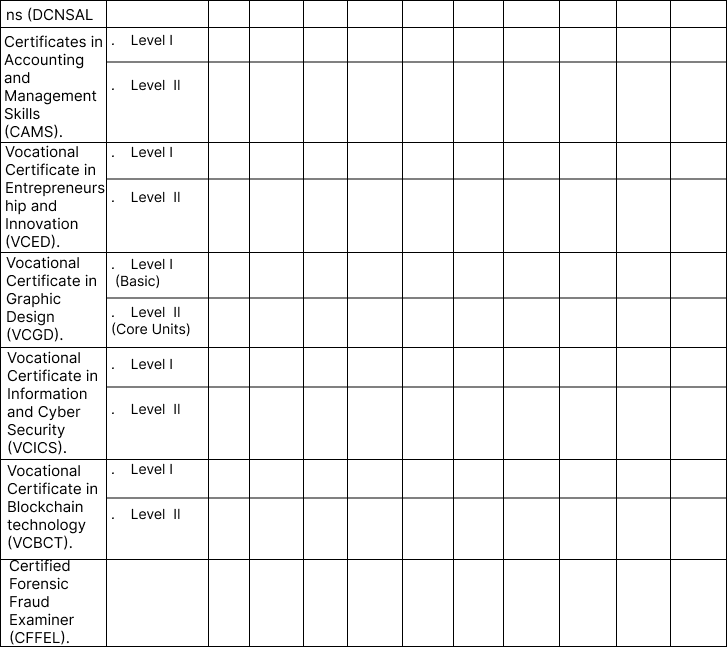

APPLICATION FORM FOR ACCREDITATION OF TRAINING INSTITUTIONS

(Universities, University colleges and campuses to complete form KAS/FM/ACC/002)

In order to enable Kasneb evaluate your institution for purposes of accreditation, you are required to complete this application form and submit it together with all supporting

documents to:

The Secretary and Chief Executive

Kasneb

P.O Box 41362-00100 NAIROBI

All the information provided in this form will be treated with confidentiality.

Please read the guidelines for accreditation carefully before completing this form.

Note: A list indicating the names, designations and qualifications of key management staff should be attached.

TRAINERS

1. Provide the following information relating to the trainers of KASNEB courses in the institution:

| (a) |

CPA, ATD and CAMS examinations.

|

International Education Standard (IES) 3 - Professional Skills and General Education requires accountancy education programmes to impart, among other skills, personal, interpersonal, communication, presentation and reporting skills (refer to the guidelines on accreditation of training institutions).

IES 4 – Professional values, ethics and attitudes requires the presentation of professional values, ethics and attitudes to students be enhanced through the use of participative approaches (refer to the guidelines on accreditation of training institutions).

| (b) |

Other subjects examinable by the Examinations Board [CFFE, CS, CIFA CCP CISSE, DDMA and DCNSA, VCBT, VCEI, ]

|

Comment on whether the training programmes in your institution comply with the requirements of IES 3 and IES 4.

...............................................................................................................................................

...............................................................................................................................................

FIFTH SCHEDULE [r. 42(13)]

ACCREDITATION FEE

|

S/No.

|

Type of Accreditation

|

Fee Payable (Kenya Shillings)

|

|

1.

|

Interim Accreditation (Eighteen months)

|

10,000.00

|

|

2.

|

Full Accreditation (Five years)

|

40,000.00

|

|

3.

|

Renewal of accreditation (Five years)

|

30,000.00

|

|

4.

|

Appeal lodgment fee

|

5,000.00

|

|

5.

|

Annual assessment fees

|

2,000.00

|

THE ACCOUNTANTS (EXAMINATIONS) RULES

PART I – PRELIMINARY

| 1. |

Citation

These Rules may be cited as the Accountants (Examinations) Rules.

|

| 2. |

Interpretation

In these Rules, unless the context otherwise requires —

“Act” means the Accountants Act (Cap. 531);

“agent” means a person either natural or artificial not being a member of staff, appointed by the Examinations Board to undertake examinations related assignments from time to time;

"accreditation" means the formal recognition and confirmation by certification that an institution has met and continues to meet the quality standards of, training and competence set by the Examinations Board in liaison with the Ministry of Education in accordance with the guidelines set out in Part III of these Rules;

“area coordinator “means an officer appointed by the County Education Officer to manage, control and handle all the examination related matters of the Examinations Board at the sub-county level during the administration of examinations;

“attempt timer” means a clock indicating the time limit for starting the examination offered by the Examinations Board;

"Cabinet Secretary" has the meaning assigned to it under section 2 of the Act;

“candidate” means a natural person who has been registered by the Examinations Board and has been entered for an examination;

“chief invigilator” means an officer appointed by the Examinations Board to manage, control and handle all the examination related matters of the Examinations Board at the assigned examinations centre during the administration of examinations;

“computer-based examinations” means an examination that is conducted online through the use of internet or a computer-aided facility;

“Examinations Board” has the meaning assigned to it under section 2 of the Act;

“examination centre coordinator” means officer appointed by the Examinations Board and designated as an examinations centre coordinator to coordinate logistical matters at the examinations centre during the administration of an examination;

“examination materials” means any materials and or equipment made available by the Examinations Board to a candidate during an examination, including but not limited to examination question papers and examination answer booklets;

"examination timer" means a computer clock that shows current, start and finish time with countdown set in hours and minutes to let candidates know how much time is left while taking examinations;

"institution" means an institution accredited to offer training in subjects examinable by the Examinations Board;

"online remote proctored examinations" means computerized examinations conducted through Examinations Board’s online examination portal, during which a candidate is monitored virtually and in real time by an online proctor, and for which control and monitoring also takes place afterwards, on the basis of video and audio recordings made during the examination;

“online proctor” means a person tasked with invigilating online exams via Webcam;

“professionals’ examination” means any examination offered by the Examinations Board which is classified under category seven of qualification pathways issued by the Kenya National Qualifications Authority in accordance with the Kenya National Qualifications Framework Act (Cap. 214) or any other qualification set out by the International Federation of Accountants or any other regulatory body, locally or internationally;

“registered student” means a student who having met all the entry requirements set by the Examinations Board for any of its examinations, has been duly registered and has a registration number;

“supervisor” means an employee of the Examinations Board or employee of Government deployed to monitor the conduct and administration of examinations within a given examination centre or group of centres;

“technicians’ examination” means any examination offered by the Examinations Board which is below the professional examination and includes but is not limited to vocational, certificate and diploma examinations; and

“webcam” means a video camera that feeds or streams an image or video in real time to or through a computer to a computer network, such as the internet.

|

| 3. |

Objects and purpose

The objects and purpose of these Rules is to govern matters relating to the administration, management and conduct of examinations offered by institutions and accreditation of institutions by the Examinations Board in accordance with the Act.

|

PART II – EXAMINATIONS RULES

| 4. |

Scope of the Rules

These Rules provide for the following —

| (a) |

development and review of syllabi for examinations offered by the Examinations Board;

|

| (b) |

accreditation of institutions offering training in subjects examinable by the Examinations Board;

|

| (c) |

administration, management and conduct of examinations of the Examinations Board;

|

| (d) |

examinations’ irregularities and the penalties thereof;

|

| (e) |

issuance of certificates by the Examinations Board;

|

| (f) |

exemption and equation of certificates including prescribing what examinations may be equated by the Examinations Board in liaison with the Commission for University Education, Technical and Vocational Education and Training Authority, Kenya National Qualifications Authority or any other relevant statutory body;

|

| (g) |

examination fees and other charges payable to the Examinations Board; and

|

| (h) |

approval of publication of books and other materials relevant to examinations offered by the Examinations Board.

|

|

| 5. |

Registration requirements

| (1) |

A person shall be deemed to have been registered as a candidate upon meeting all the entry requirements set out in these Rules and paying the registration fees.

|

| (2) |

A birth certificate shall suffice for identification purposes for registration until a candidate acquires a national identification or any other recognized document for identification.

|

| (3) |

The Examinations Board has the right to reject any application for registration for a justifiable reason.

|

|

| 6. |

Booking of examinations

| (1) |

An examination entry, which shall be in the form set out in the First Schedule, shall be accepted from a registered student.

|

| (2) |

The Examinations Board shall assign each candidate a registration number upon registration as a student of the Examinations Board.

|

| (3) |

The closing date for the receipt of entries for the various examination sittings shall be determined by the Examinations Board from time to time.

|

| (4) |

Notwithstanding the provisions of sub rule (3), the Examinations Board may extend the date of students’ registration under special circumstances.

|

| (5) |

Where the Examinations Board extends the closing date under sub rule (4), the Examinations Board —

| (a) |

shall allow adequate time for the administration of the examination;

|

| (b) |

may charge additional fees for any such late entries; and

|

| (c) |

shall keep a record of the students registered under special circumstances.

|

|

| (6) |

Once registered students have been entered for a particular examination sitting, a summary of all the registered students shall be tabled to the Board.

|

| (7) |

The Examinations Board shall circulate the register of students to the designated chief invigilator before the commencement of the particular examination sitting.

|

| (8) |

In each examination sitting, the Examinations Board shall, upon approval by the Board under sub rule (4), transmit a list of all newly registered students entered for the certified public accountant examination to the Institute, on or before twenty-one days after closure of the register.

|

|

| 7. |

Allocation of examination centres

| (1) |

The Examinations Board shall assess and identify appropriate centres for each examination sitting of the Examinations Board.

|

| (2) |

A registered student who has been entered for an examination, may select three or such other number of examination centres as may be determined by the Examinations Board in the order of priority for consideration and allocation by the Examinations Board.

|

| (3) |

The Examinations Board shall allocate examination centres to students who apply under sub rule (2) based on capacity and availability of the centres.

|

| (4) |

Despite sub rule (3), the Examinations Board shall reserve the right to transfer candidates from one centre to another centre, for the efficient administration of examinations.

|

| (5) |

Where the Examinations Board transfers a candidate to another examination centre under sub rule (4), the Examinations Board shall communicate such transfer to the candidate in writing within forty-eight hours or any other time, in the event of an emergency before an examination commences.

|

|

| 8. |

Examination sittings

| (1) |

The Examinations Board shall determine the number of examination sittings in each year and reserves the right to reschedule any or all examination sittings.

|

| (2) |

Where the Examinations Board reschedules an examination sitting under sub rule (1), the Examinations Board shall notify the affected candidates and the public within reasonable time.

|

|

| 9. |

Conduct of students in the examination room

The following rules shall govern the conduct of students in the examination room —

| (a) |

a candidate shall present himself for an examination at least thirty minutes before the scheduled time for the commencement of the examination he or she is taking;

|

| (b) |

a candidate shall identify himself or herself before being allowed to sit an examination by presenting his national identification or any other document approved by the Board to sit an examination;

|

| (c) |

a candidate who arrives more than half an hour after the commencement of an examination shall not be allowed to take the examination;

|

| (d) |

a candidate shall not be permitted to leave the examination room until after the end of the first half hour from the commencement of an examination provided that a chief invigilator may remove a candidate who is disruptive, less than the first half hour from such commencement;

|

| (e) |

a candidate shall sit at the place indicated by the assigned registration number in the examination room;

|

| (f) |

a candidate shall indicate his registration number on the answer sheet;

|

| (g) |

a candidate shall not insert his name on the answer sheet;

|

| (h) |